Do you know how the 2020 to 2022 National AgriStability Program changes impact your farm?

Do you know how the 2020 to 2022 National AgriStability Program changes impact your farm?

Find out how changes to the 2020 to 2022 National AgriStability Program could impact your farm with our detailed overview.

Removal of reference margin limiting (RML) – Producers and sectors which had low to moderate AgriStability eligible costs and corresponding limited reference margins will benefit from higher reference margins and better coverage.

Revenue trigger points vary significantly by type of farm, but now with RML removed, they are always less than 30 percent. Knowing this helps producers make better risk management decisions by including AgriStability as the cornerstone of their risk management plan.

Treatment of private insurance proceeds – Proceeds from Livestock Price Insurance, private hail, GARS and Just Solutions will no longer offset AgriStability payments, but they continue to be included in reference margins, helping to maximize payment potential.

This means producers can potentially double up on coverage if they take AgriStability and private insurance. The change in treatment of private insurance proceeds is something that producers should seriously consider when evaluating and determining their annual insurance risk management strategy.

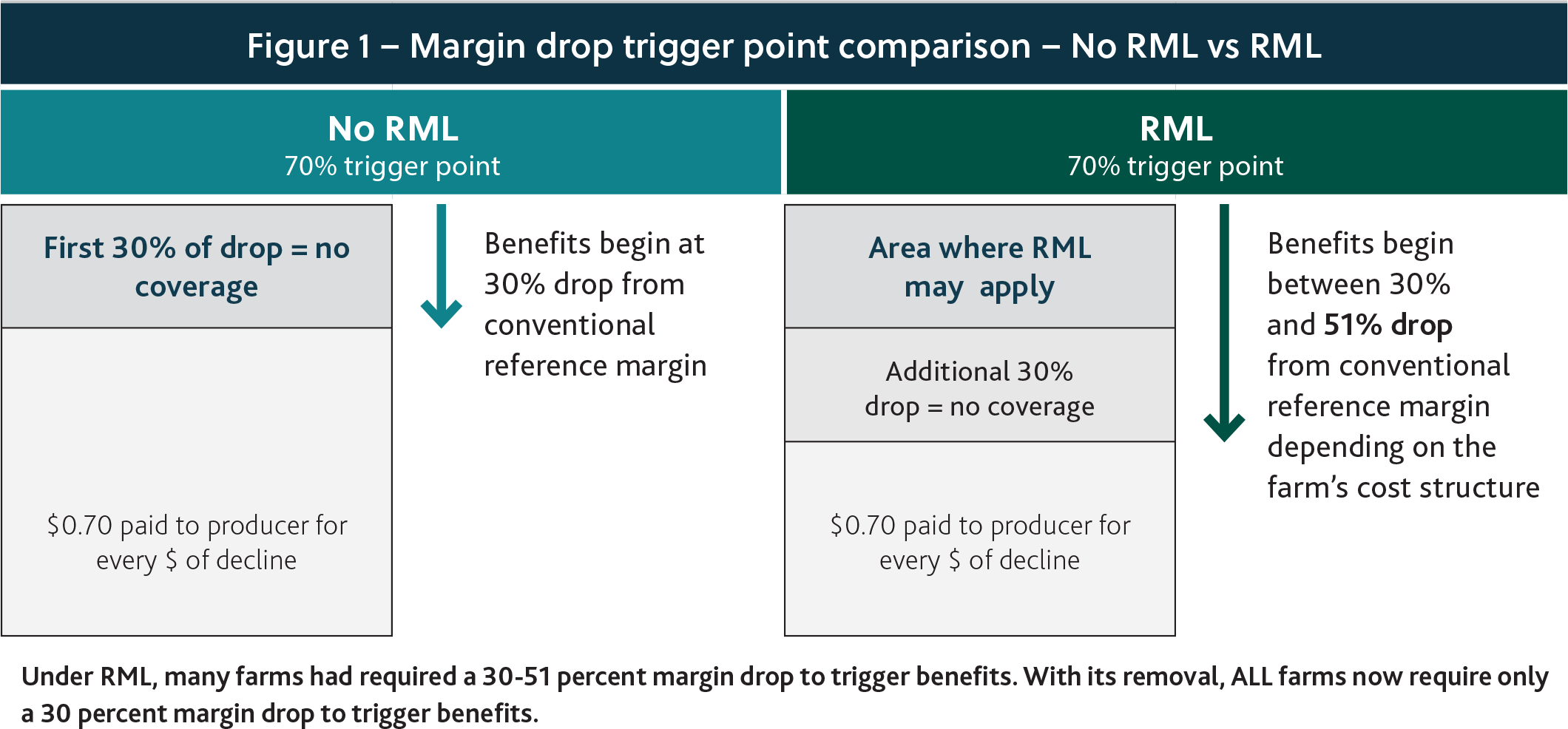

Figure 1 below illustrates the difference between margin trigger points with no RML vs RML. The two larger rectangles represent the reference margin for a farm. The example shaded in teal shows a reference margin with no RML and the fact that AgriStability benefits begin only after there has been a 30-percent drop relative to that reference margin. Once the farm drops into the payment zone, the producer is paid 70 cents for every dollar of decline.

The example shaded in green shows a potentially limited reference margin. The limiting could apply anywhere in the portion of the rectangle that is marked “Area where RML may apply.” If RML applied, the producer had to have a drop of 30 percent from that limited margin to qualify for the 70 cents per dollar of AgriStability benefits.

The most important thing to understand is that RML increased the margin drop required to trigger benefits substantially when we relate it back to the original reference margin. Specifically, farms for which RML applied required a 30 – 51 percent drop, depending on degree of limiting, relative to their original reference margin to trigger AgriStability benefits. That is what made the program so much less responsive when RML applied.

Under RML, many farms had required a 30 – 51 percent margin drop to trigger benefits. With its removal, ALL farms now require only a 30-percent margin drop to trigger benefits.

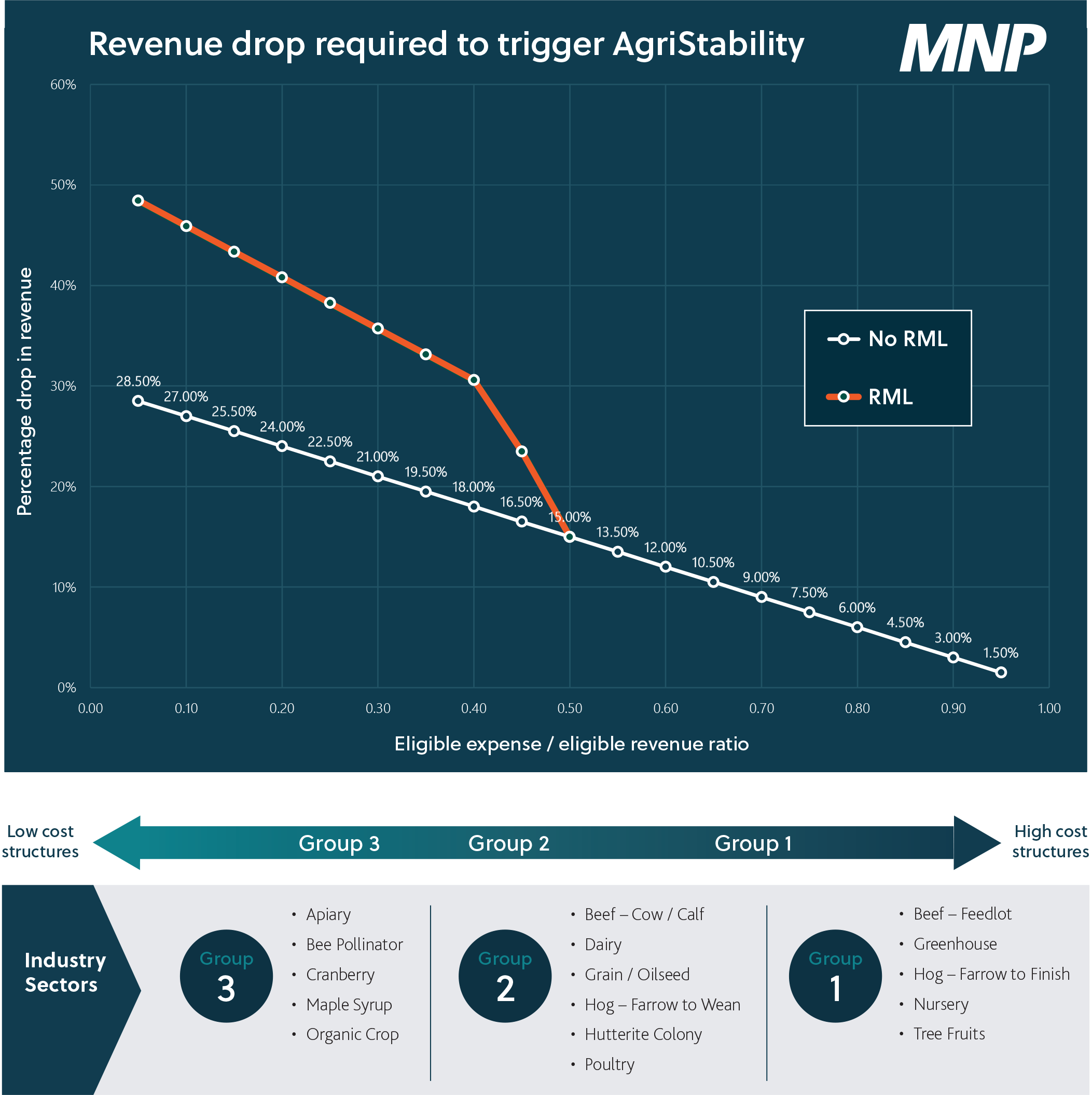

Figure 2 below examines the cost structure for various farming sectors and shows how cost structure relates to the responsiveness of the AgriStability program. In Figure 2, we highlight the revenue trigger points required to trigger AgriStability for various types of farms. Revenue trigger points represent the drop in revenue (through production loss, price loss or a combination of both) required to trigger AgriStability. We have found that revenue trigger points are easier for producers to relate to than margin trigger points, because most farm disasters have a significant revenue loss component. Without RML, the margin trigger point becomes 30 percent for all types of farms (formerly 30 – 51 percent for farms where RML applied). However, as you will see in Figure 2, the revenue trigger points can vary significantly by type of farm, but they are always less than 30 percent and often substantially less than 30 percent. Knowing this helps producers make better risk management decisions by including AgriStability as the cornerstone of their risk management plan. It also helps producers who may have dropped out of the AgriStability program in the past, whether due to perceived impacts of RML or otherwise, visualize that they should probably get back in going forward.

Questions you might be asking yourself on the revenue trigger point graph in Figure 2

Q: Doesn’t AgriStability require a 30-percent revenue drop for any farm to trigger benefits?

A: No, the 30-percent drop advertised by the AgriStability Program is a drop relative to your reference margin. The revenue drop required varies depending on the type of farm and cost structure. Revenue drop percentages are labelled along the line graph with very low revenue drops in the bottom right hand corner and higher revenue drops on the left-hand side of the graph.

Q: Where would different types of farms fit on this graph and what kind of revenue drops would they require to trigger AgriStability benefits?

A: Farms with a high cost structure (Industry Sectors Group 1) fit on the bottom right hand side and require a revenue drop of 1.5 - 12 percent to trigger AgriStability benefits. Moving left on the graph, farms with a moderate cost structure (Industry Sectors Group 2) require an estimated 12 - 19.5 percent revenue drop, and those with a low-cost structure (Industry Sectors Group 3) require an estimated 19.5 - 25.5 percent revenue drop.

Q: What difference does knowing the revenue drop required to trigger AgriStability benefits make for me?

A: It is critical that you know and understand what level of revenue drop is required, as well as what risks might contribute to a revenue drop for your operation to make a proper decision on AgriStability participation.

Q: What difference did removal of the RML have on the revenue drops required to trigger AgriStability benefits?

A: The orange line (labelled RML) on the graph, when compared to the white line (labelled No RML), shows the potential impact RML had on revenue drop trigger points for certain farms in Group 2 and Group 3. Certain farms in these sectors will benefit from substantially lower revenue drop trigger points now that RML has been removed.

Q: How would I go about figuring out the eligible expense to eligible revenue ratio to determine where my farming operation would fit on this graph?

A: Eligible revenue and eligible expense are both defined by AgriStability program rules. Ideally, you would have to know the average eligible revenue and eligible expense from the three years used to calculate your Olympic Average reference margin for AgriStability. These amounts can be estimated using the most recent AgriStability Calculation of Program Benefits (COB) notices and / or accrued financial statements.

Estimation of AgriStability reference margins, particularly if you have not participated in AgriStability recently or if you do not have up to date COBs, can be difficult for a number of reasons. We would recommend the estimates not be undertaken without the assistance of an advisor who is proficient in AgriStability policy and procedures.

Treatment of private insurance proceeds

For the 2020 to 2022 years, treatment of private insurance proceeds for the AgriStability program year has changed. Private insurance proceeds, including Livestock Price Insurance, private hail, GARS and Just Solutions, are not treated as eligible revenue in the program year. This means receiving private insurance will not reduce AgriStability benefits, allowing producers to potentially double up on coverage if they take AgriStability and private insurance.

Treatment of private insurance proceeds in the reference margin calculations is not changing and they are still included in the reference margin as eligible revenue. This keeps the reference margins higher, thereby maximizing future payment potential for those producers who may have benefitted from private insurance payments in the past. Treatment of private insurance premiums is also not changing, and they will remain as eligible expense in both the reference and program year margins, meaning they are potentially covered by the AgriStability program. The change in treatment of private insurance proceeds is something producers should seriously consider when evaluating and determining their annual insurance risk management strategy.

Next steps

The 2021 AgriStability Enrolment Deadline has been extended from April 30 to June 30, 2021. Contact your local Business Advisor to enroll if you have either previously opted out of or never participated in the AgriStability program. Enrolment has been simplified for returning participants; now you have a choice to base your coverage.

Visit MNP.ca/ARMR to watch a short video further explaining the AgriStability changes.

Insights

-

October 28, 2025

How can an ESOP support your succession goals? These considerations can help you understand if an ESOP is the right strategy for your construction business.

-

Confidence

October 27, 2025

The VDP is a valuable opportunity for Canadians to correct past tax filing errors. Recent changes have made it more accessible and increased the relief available.

-

Performance

October 23, 2025

When performance falters, acting early can preserve value. Learn how five strategies helped one company avoid insolvency and secure recovery.